TOCALO Co., Ltd. (TSE: 3433): Stock Analysis

August 17, 2025

1. Introduction

Tocalo Co., Ltd. (TSE: 3433) is Japan’s leading thermal spraying company, providing surface treatment services to a wide range of industries including semiconductors, aerospace, power generation, and steelmaking. Leveraging its proprietary spraying technologies such as ceramics, cermet, and metallic coatings, Tocalo plays a critical role in improving the durability, performance, and heat resistance of high-value industrial components.

With its headquarters in Kobe and a global presence spanning Asia and the U.S., the company is a key enabler of downstream manufacturing and energy efficiency. As of August 15, 2025, the company is valued at ¥2,041 per share, reflecting renewed investor interest following operational expansion and capital efficiency improvements.

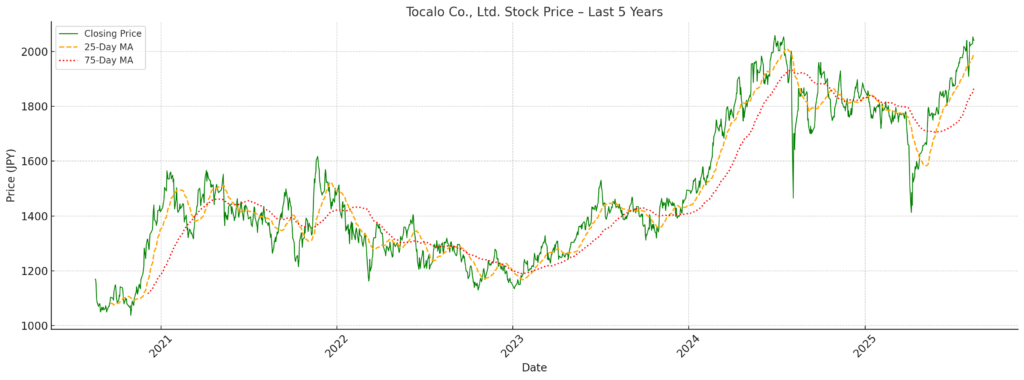

2. Stock Price Performance

| Latest Price | ¥2,041 (Aug 15, 2025) |

| 52-Week High | ¥2,160 |

| 52-Week Low | ¥1,761 |

| Average Price (1Y) | ~¥1,950 |

| Change from Low | +15.9% |

| Change from High | -5.5% |

The stock has shown a moderate recovery from its lows in 2024, supported by stable earnings and a consistent dividend policy. Although the price remains slightly below the 52-week high, valuation metrics remain reasonable, suggesting upside potential amid favorable industrial trends.

3. Financial and Operational Performance

Tocalo achieved a strong financial turnaround in FY2025, regaining growth momentum after a temporary decline in FY2024. The performance highlights the company’s operational resilience and strategic positioning in high-value industrial coatings.

3.1 Overview of Key Financial Metrics (Consolidated)

| Fiscal Year | Revenue (¥mn) | Operating Profit (¥mn) | OPM (%) | Net Profit (¥mn) | EPS (¥) | DPS (¥) |

|---|---|---|---|---|---|---|

| FY2023 | 48,144 | 10,558 | 21.9% | 7,350 | 120.83 | 50 |

| FY2024 | 46,735 | 9,197 | 19.7% | 6,326 | 105.53 | 53 |

| FY2025 | 54,231 | 12,271 | 22.6% | 8,052 | 135.45 | 68 |

Highlights:

Revenue increased by +16.0% YoY, reaching a record high. The key growth drivers were:

Semiconductor-related demand rebound (both domestic and Taiwan-based customers)

Strength in clean energy, power generation, and industrial machinery segments

Price adjustments to pass through elevated input costs

Operating Profit rose by +33.5% YoY, reflecting:

Higher capacity utilization at key plants (notably for thermal barrier coatings)

Stabilization of raw material prices (e.g., metal powders, fuel gases)

Improved productivity through automation and digitalization efforts

Net Profit Margin recovered to 14.8% (vs. 13.5% in FY2024), supported by lower extraordinary losses and stable financial expenses.

3.2 Segment Analysis

Tocalo’s operations are not formally segmented by business unit in accounting disclosures, but internal reporting classifies performance broadly as follows:

| Segment | FY2025 Trend | Commentary |

|---|---|---|

| Semiconductor/Display | Significant YoY growth | Recovery in capex from key Japanese and Taiwanese chipmakers; continued demand for plasma-resistant coatings and thermal spray |

| Energy / Power Systems | Stable to modest growth | Maintenance and refurbishment demand from utilities; high durability coatings in thermal and nuclear power sectors |

| General Industrial | Moderate recovery | Resumption of machinery upgrades and demand for abrasion-resistant coatings in steel, paper, and food industries |

3.3 Geographic Performance

| Region | Commentary |

|---|---|

| Japan | Core market; accounts for ~70% of revenue. Stable public and private sector demand. |

| Taiwan | Strong double-digit growth, mainly from semiconductor clients. |

| Southeast Asia | Early-stage growth, with high expectations tied to new plant investments. |

The overseas business share has now exceeded 25%, and the company aims to grow this to over 30% in the medium term.

3.4 Productivity and Cost Structure

Material Cost Ratio: Improved slightly as metal material inflation normalized

Labor Productivity: Benefited from automation and shift-based line operations

Capex Efficiency: Higher depreciation offset by top-line growth; strategic investments in plasma spraying and HVOF equipment are yielding margin leverage

3.5 Shareholder Returns and Balance Sheet

Dividend Growth: From ¥53 in FY2024 to ¥68 in FY2025 (+28% YoY), reflecting profit recovery and management’s policy to maintain 50–60% payout ratio.

Financial Stability:

Net cash position remains solid; essentially debt-free

Equity ratio: ~85%

ROE: Recovered to ~13.3% (vs. 11.3% in FY2024)

3.6 Year-on-Year Comparison Summary

| Factor | FY2024 | FY2025 | Remarks |

|---|---|---|---|

| Revenue | Decrease due to delayed orders and cost pass-through lag | Rebound in orders and successful pricing actions | Semiconductor cycle bottomed out |

| Profitability | Squeezed by material cost inflation and energy surges | Recovery from fixed-cost leverage and efficiency gains | Positive operating leverage |

| Shareholder Returns | Modest dividend increase | Aggressive hike to ¥68 | Reflects confidence in sustainability of earnings |

4. Strategic Initiatives

The company’s Mid-term Management Plan (FY2023–FY2025) focuses on:

Capacity Expansion: New facilities in Saga, Hiroshima, and enhanced U.S. operations (Phoenix site).

Smart Factory Transformation: Implementation of IoT/AI to streamline coating processes.

Global Market Development: Investment in ASEAN and US market penetration.

Sustainability & Governance: Strong commitment to ESG via CO₂ reduction and fair governance (75%+ of board are independent/external).

5. Growth Drivers and Catalysts

5.1 Growth Drivers

Semiconductor Supply Chain Localization: Increased demand for domestic equipment in Japan and U.S. fabs.

Decarbonization: High-performance coatings used in hydrogen and renewable energy infrastructure.

U.S. Market Strategy: Revenue contribution from U.S. subsidiary is increasing (FY2024: +40% YoY).

M&A Readiness: Solid balance sheet allows strategic acquisitions of niche surface treatment firms.

5.2 Near-Term Catalysts

Ramp-up of new Saga and Hiroshima plants

Tailwinds from FY2026/03 full-year impact of smart factory initiatives

Potential upside from the U.S. subsidy ecosystem (CHIPS Act-related orders)

6. Risks

| Type | Description |

|---|---|

| FX Risk | Revenue from overseas subsidiaries is subject to yen appreciation pressure. |

| Semiconductor Cyclicality | Exposure to capex slowdown in semiconductor sector. |

| Technical Talent Shortage | Engineering talent for thermal spray remains limited. |

| Capex Execution | Delays in new plant operationalization could hurt margins. |

7. Conclusion

Where we stand:

Tocalo has demonstrated consistent operational resilience and strategic focus, as reflected in its stable margins, robust financial structure (equity ratio ~86%), and disciplined capital allocation. The company’s medium-term plan (FY2024–FY2026) targets ¥60 billion in sales and ¥15 billion in operating profit by FY2026, implying an achievable CAGR of 4.7% and profit margin of 25%. With FY2026 EPS forecast at ¥140.11, the company continues to show earnings reliability.

Valuation Considerations:

As of August 2025, Tocalo’s stock trades at approximately ¥2,120, which implies the following valuation metrics:

| Metric | Value | Note |

|---|---|---|

| EPS (FY2026E) | ¥140.11 | Company forecast |

| PER (Forward) | ~15.1× | Reasonable given stable ROE |

| PBR | ~2.0× | Reflects strong capital base |

| Dividend Yield | ~3.3% | Consistent with historical range |

Compared to domestic peers in surface treatment and industrial equipment components, Tocalo’s valuation is moderate to slightly discounted, particularly given its niche dominance in thermal spraying and strong financial profile.

Investment Judgment:

Rating: Accumulate (Long-Term Buy)

Rationale: Tocalo presents a well-managed, niche industrial company with stable earnings, improving shareholder returns, and long-term strategic clarity. While the stock may not offer explosive growth, it is a compelling candidate for value-oriented investors seeking steady compounding in Japan’s precision manufacturing sector.

Upside Catalysts: Better-than-expected margin expansion, international sales growth, or M&A-driven scale-up.

Risks: Demand volatility in semiconductor or energy sectors, execution delays in growth projects, and inflationary cost pressures.

In sum, Tocalo offers a balance of stability and strategic upside — a quiet compounder in Japan’s high-precision industrial space.

At Wasabi Info, we publish concise equity reports and market insights through our blog—

but our core value lies in providing bespoke, on-demand research for international clients.

Whether you are a private investor or a corporation, we deliver confidential, tailored intelligence designed to support strategic decisions.

Our research services include:

• Equities: In-depth analysis of Japan-listed companies not featured in the blog

• Competitor Analysis: Detailed mapping of industry rivals and market dynamics

• Market Entry Intelligence: Insights into local barriers, regulations, and competitor positioning

• Real Estate & Assets: Localized assessments for factory, hotel, or retail expansion

• Field Intelligence: On-the-ground surveys and discreet market checks unavailable through public sources

Reports are available in English, Chinese, and Japanese.

For inquiries, please contact: admin@wasabi-info.com

© Wasabi Info | Privacy Policy

Disclaimer

This report is intended for informational purposes only and does not constitute investment advice. The analysis contains forward-looking statements and interpretations based on publicly available information as of the date of writing. Readers should conduct their own research and consult with a licensed financial advisor before making any investment decisions.

Wasabi-Info.com shall not be held liable for any loss or damage arising from the use of this report or reliance on its contents.