Dai-Ichi Cutter Kogyo K.K. (TSE: 1716): Stock Analysis

August 18, 2025

1. Introduction

Dai-Ichi Cutter Kogyo Co., Ltd. (TSE: 1716) is a leading Japanese provider of demolition, concrete cutting, hydro-demolition, and preventive infrastructure maintenance services. With deep expertise in high-precision, high-safety work, the company plays a critical role in Japan’s aging public infrastructure landscape. Its business model focuses on safety, environmental compliance, and efficiency—supported by proprietary technologies and a highly skilled workforce.

2. Stock Price Performance

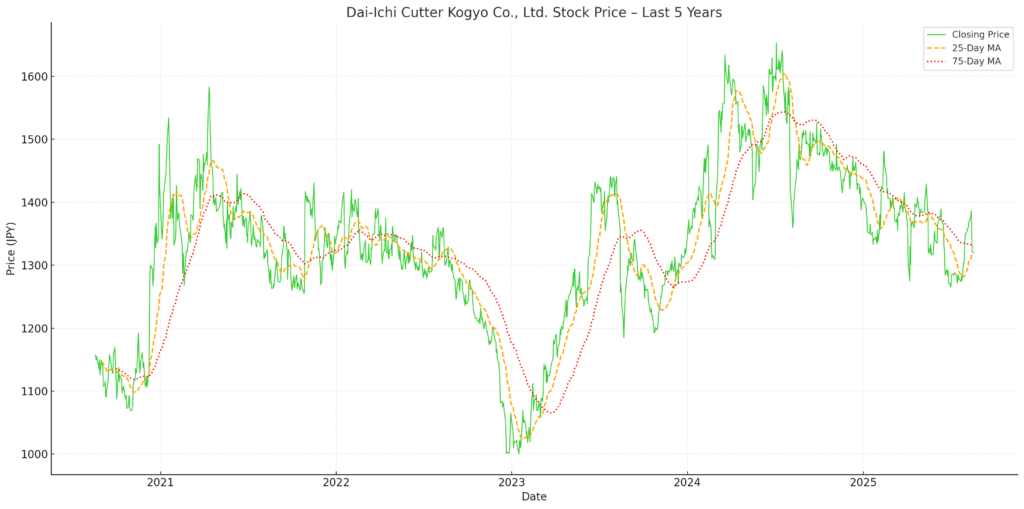

Over the past 14 months, Dai-Ichi Cutter’s stock experienced a notable peak in mid-2024 followed by a steady decline.

Recent High: The stock reached a record high of ¥1,653 on July 4, 2024.

August 2025: As of August 18, 2025, the stock has retreated to ¥1,320, reflecting a total decline of roughly 20% from the peak.

Decline Considerations (July 2024 – August 2025):

Weaker-than-expected FY2024 results announced in August 2024 revealed revenue and operating profit declines, breaking the prior growth trajectory.

Execution delays in scaling preventive maintenance services, a core pillar of the company’s medium-term strategy, raised doubts about near-term earnings upside.

Loss of investor momentum following the FY2023 earnings optimism and subsequent peak in July 2024.

Broader market rotation away from small/mid-cap construction names amid rising macro uncertainty and muted public-sector spending.

Valuation de-rating as growth visibility temporarily weakened, despite solid fundamentals.

The downward trend reflects investor reassessment of short-term earnings momentum, even though long-term structural demand for infrastructure maintenance remains intact.

3. Financial and Operational Overview

Key Financial Metrics (JPY million)

| Fiscal Year | Revenue | Operating Profit | Net Income | EPS (¥) | Dividend (¥) | OP Margin | Net Margin |

|---|---|---|---|---|---|---|---|

| FY2022 | 20,949 | 2,502 | 1,580 | 138.8 | 28 | 11.9% | 7.5% |

| FY2023 | 22,164 | 2,631 | 1,946 | 172.0 | 35 | 11.9% | 8.8% |

| FY2024 | 20,918 | 2,455 | 1,973 | 174.4 | 38 | 11.7% | 9.4% |

Analysis:

Revenue declined by 5.6% in FY2024 due to completion of large public projects and slow ramp-up of new services.

Operating profit fell by 6.7%, impacted by fixed cost absorption pressure and higher parts/materials costs.

Net income rose slightly, supported by tax efficiency and cost control, pushing net margin to 9.4%.

Margins remained resilient despite topline contraction, highlighting operational stability.

ROE is stable near 9.8%, and equity ratio improved to ~67%.

Capital Allocation:

Capital expenditures focused on battery-powered equipment and automation.

DPS has steadily increased: ¥28 → ¥35 → ¥38, aligning with the mid-term goal of a ≥30% payout ratio.

4. Strategic Positioning & Medium-Term Plan (FY2025–FY2027)

Dai-Ichi Cutter’s Medium-Term Management Plan (announced in 2024) aims to transform the company into a high-efficiency, technology-enabled infrastructure specialist by FY2027.

FY2027 Targets:

Revenue: ¥24.5 billion

Operating Profit: ¥2.45 billion

ROE: >10%

Dividend Payout: ≥30%

Strategic Focus Areas:

Growth in preventive maintenance (recurring services vs. one-off demolition)

Investment in DX, AI, and automation technologies

Expansion into non-metropolitan markets via M&A

Development of next-generation cutting and surface treatment systems

Upskilling and training programs to address labor shortages

5. Competitive Advantages

Japan’s top share in high-precision concrete cutting and hydro-demolition

Proprietary equipment fleet and method patents enhance efficiency and safety

Deep trust from public infrastructure clients (bridges, tunnels, plants)

Early adoption of robotics and DX, boosting productivity amid labor shortages

Broad regional footprint across Japan

6. Risks

| Risk | Description |

|---|---|

| Revenue Volatility | Project-based revenue timing impacts earnings smoothness |

| Labor Constraints | Skilled labor availability remains a challenge in the sector |

| Technology Execution | AI/DX initiatives may underperform or face delays |

| M&A Integration Risk | Acquired entities may not achieve intended synergies |

| Limited Global Diversification | Business is almost entirely domestic |

7. Conclusion

Despite short-term pressure in FY2024, Dai-Ichi Cutter remains structurally strong. The shift toward preventive maintenance and automation is strategically sound, but the pace of monetization has lagged investor expectations.

At ¥1,320, valuation metrics are appealing:

| Metric | Value |

|---|---|

| P/E (FY2024) | ~7.6× |

| P/B | ~0.8× |

| Dividend Yield | ~2.9% |

| ROE | ~9.8% |

These suggest a moderately undervalued stock, particularly for defensive portfolios. While FY2025 may be transitional, the company’s earnings quality, capital discipline, and niche positioning support long-term upside.

Investment Verdict:

HOLD to MODERATE BUY

For investors seeking:

Stable dividends

Infrastructure exposure

Long-term DX-enabled transformation

At Wasabi Info, we publish concise equity reports and market insights through our blog—

but our core value lies in providing bespoke, on-demand research for international clients.

Whether you are a private investor or a corporation, we deliver confidential, tailored intelligence designed to support strategic decisions.

Our research services include:

• Equities: In-depth analysis of Japan-listed companies not featured in the blog

• Competitor Analysis: Detailed mapping of industry rivals and market dynamics

• Market Entry Intelligence: Insights into local barriers, regulations, and competitor positioning

• Real Estate & Assets: Localized assessments for factory, hotel, or retail expansion

• Field Intelligence: On-the-ground surveys and discreet market checks unavailable through public sources

Reports are available in English, Chinese, and Japanese.

For inquiries, please contact: admin@wasabi-info.com

© Wasabi Info | Privacy Policy

Disclaimer

This report is intended for informational purposes only and does not constitute investment advice. The analysis contains forward-looking statements and interpretations based on publicly available information as of the date of writing. Readers should conduct their own research and consult with a licensed financial advisor before making any investment decisions.

Wasabi-Info.com shall not be held liable for any loss or damage arising from the use of this report or reliance on its contents.