Sumitomo Forestry Co., Ltd. (TSE: 1911): Stock Analysis

August 27, 2025

1. Introduction

Sumitomo Forestry Co., Ltd., established in 1691, has evolved from its origins as a forestry operator for the Sumitomo family’s copper mine into a diversified global enterprise encompassing forestry management, timber and building materials, housing construction, real estate development, and renewable energy. Unlike peers focused solely on housing or construction, the company differentiates itself through its integrated value chain, the “Wood Cycle,” which links sustainable forest management with timber utilization and renewable energy. This model aims to deliver both financial returns and environmental value, positioning the company as a rare case of a housing and construction group with a clear decarbonization strategy.

Today, the group is a multinational operator with significant exposure to Japan, the United States, and Australia. It has gained scale through acquisitions such as Henley and Metricon in Australia and Brightland Homes in the U.S., while reinforcing its domestic housing business with a focus on energy-efficient homes and large-scale wooden buildings. At the same time, it is expanding renewable energy and forestry-related businesses, contributing to the global shift toward carbon neutrality.

This report provides a comprehensive analysis of Sumitomo Forestry for global investors. It reviews the company’s stock price development, financial and operational performance over the past three years (2022–2024), and strategic outlook under the mid-term plan Mission TREEING 2030 Phase 2. It also examines the key risks and catalysts that may influence future performance and concludes with a balanced view on valuation and investment considerations at the current share price.

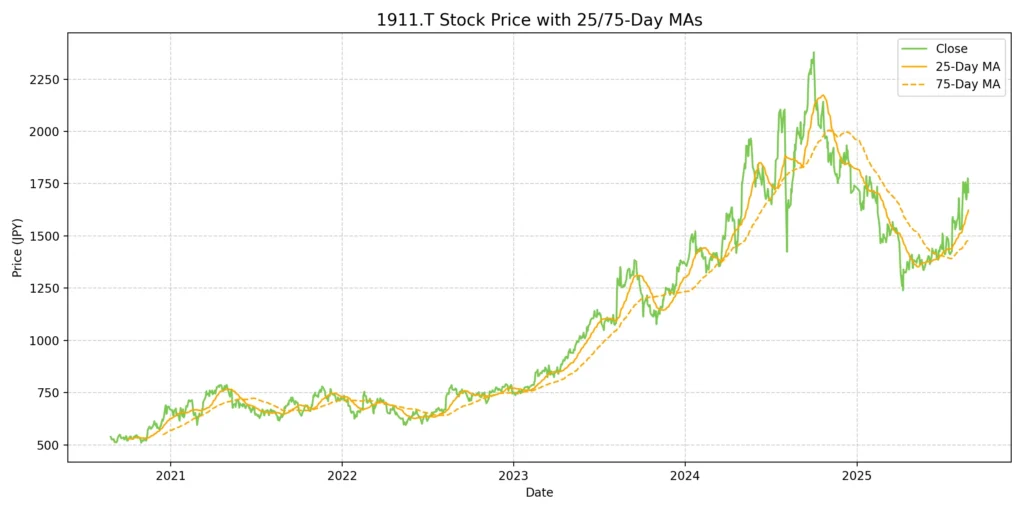

2. Stock Price Development

Sumitomo Forestry’s stock has historically mirrored both cyclical housing demand and long-term ESG themes.

Current Price (Aug 2025): ~¥1,678

52-week Range: ¥1,221 – ¥2,431

Market Capitalization: ~¥700 bn

PER (based on FY2024 EPS): ~2.9x

Dividend Yield (based on FY2024 DPS): ~8.6%

Performance Review:

In 2022–2023, shares underperformed due to the U.S. housing slowdown caused by mortgage rates exceeding 7%. In 2024, optimism over the acquisition of Metricon in Australia, combined with record revenues, drove the stock to over ¥2,400. Since early 2025, the stock has corrected back to the ¥1,700 range, reflecting uncertainty over the pace of U.S. housing recovery.

Relative Context:

TSR (Total Shareholder Return) has generally outpaced TOPIX over the past decade, supported by dividend growth. Current valuation levels are extremely low on earnings and book value multiples, reflecting both potential undervaluation and market caution over the sustainability of profits.

3. Financial and Operational Performance (FY2022–2024)

3.1 Key Financial Metrics

| Fiscal Year | Revenue (¥bn) | Operating Profit (¥bn) | Net Income (¥bn) | Total Assets (¥bn) | Net Assets (¥bn) | ROE (%) | EPS (¥) | DPS (¥) |

|---|---|---|---|---|---|---|---|---|

| 2022 | 1,669.7 | 158.3 | 108.7 | 1,537.6 | 682.6 | 19.4 | 543.8 | 125 |

| 2023 | 1,733.2 | 146.8 | 102.5 | 1,812.7 | 823.3 | 14.8 | 505.5 | 125 |

| 2024 | 2,053.7 | 194.6 | 116.5 | 2,261.1 | 1,020.1 | 13.9 | 569.4 | 145 |

Sources: Securities Reports (FY2022–2024).

3.2 Observations

Between FY2022 and FY2024, Sumitomo Forestry demonstrated resilience with stable profitability and growing scale, though returns on equity moderated as capital expanded faster than earnings.

Revenue Growth:

Revenue increased from ¥1,669.7 bn (2022) to ¥2,053.7 bn (2024), a three-year growth of approximately +23%.

Growth was supported by expansion in overseas housing, especially in Australia, where the acquisition of Metricon in FY2024 significantly enlarged the company’s presence.

Operating Profit Trends:

Operating profit declined from ¥158.3 bn in 2022 to ¥146.8 bn in 2023, reflecting headwinds in the U.S. housing market, where rising mortgage rates (~7%) reduced affordability, and competitive pricing pressure intensified.

In FY2024, operating profit rebounded strongly to ¥194.6 bn, supported by stable domestic housing demand, disciplined cost control, and consolidation of overseas subsidiaries including Metricon.

Net Income and EPS:

Net income remained consistently above ¥100 bn across the period, highlighting the stability of the business model.

Results were ¥108.7 bn in 2022, ¥102.5 bn in 2023, and ¥116.5 bn in 2024. EPS followed this trend, recovering to a three-year high of ¥569.4 in 2024.

Balance Sheet Expansion:

Total assets rose from ¥1,537.6 bn in 2022 to ¥2,261.1 bn in 2024, driven by overseas acquisitions and business growth.

Net assets expanded from ¥682.6 bn to ¥1,020.1 bn, reflecting retained earnings and equity financing.

ROE Decline:

ROE fell from 19.4% in 2022 to 13.9% in 2024, indicating that equity growth has outpaced profit growth.

While this reflects stronger capitalization, it also signals challenges in maintaining previous levels of capital efficiency.

Dividends:

DPS was held at ¥125 in both 2022 and 2023, before being raised to ¥145 in 2024.

According to the Integrated Report 2025, the company prioritizes stable shareholder returns with a policy of 30%+ payout ratio and a dividend floor, providing predictability for long-term investors.

Overall Observation:

The company delivered robust top-line growth and resilient net income despite U.S. housing headwinds. However, declining ROE highlights a need for improved capital efficiency. Overseas expansion, particularly in Australia, has significantly increased the company’s scale but also elevated balance sheet size, making sustained profit growth critical to justify equity expansion.

4. Strategic Outlook

Under Mission TREEING 2030 Phase 2 (2025–2027), Sumitomo Forestry aims to achieve revenue exceeding ¥3 trillion and recurring profit of ¥350 bn by FY2027. The plan emphasizes both growth and decarbonization.

Global housing remains the largest driver, with U.S. housing demand expected to recover once interest rates stabilize, and Australian operations expected to deliver steady growth with Henley (an Australian homebuilder consolidated into the group in 2009) and Metricon integration. In Europe, the company is exploring opportunities in large-scale wooden commercial buildings.

The ESG strategy is central to the company’s long-term positioning. Beyond expanding its managed forest area to 1 million hectares by 2030, Sumitomo Forestry is investing in renewable energy projects such as biomass power generation and sustainable aviation fuel (SAF). These initiatives not only support global decarbonization but also provide potential new revenue streams and risk diversification. The company is also committed to RE100, targeting 100% renewable energy use across its operations. Together, these measures reinforce its dual identity as both a cyclical housing player and a sustainability-oriented enterprise.

5. Risks and Catalysts

5.1 Catalysts

Recovery in U.S. housing market as mortgage rates ease.

Expansion in Australia with Metricon delivering synergies.

Rising monetization of carbon credits from forestry assets.

Global policy support for low-carbon construction materials such as timber.

5.2 Risks

Prolonged weakness in U.S. housing if interest rates remain high.

FX volatility (USD/JPY, AUD/JPY) impacting overseas earnings.

Lumber price fluctuations compressing margins.

Execution risks in integrating acquisitions and scaling renewable energy.

Natural disasters and stricter ESG regulations.

6. Conclusion

Sumitomo Forestry’s recent financial performance illustrates both its strengths and its challenges. Between FY2022 and FY2024, revenue expanded by +23% to exceed ¥2 trillion, and net income consistently remained above ¥100 bn. The company demonstrated resilience through diversification across domestic housing, U.S. operations, Australian subsidiaries, and stable contributions from forestry and renewable energy. Dividends were maintained and then raised to ¥145 per share in FY2024, reflecting a commitment to shareholder returns.

At the same time, capital efficiency has weakened. ROE declined from 19.4% in 2022 to 13.9% in 2024, as equity expanded faster than earnings. Balance sheet growth has been significant, with net assets surpassing ¥1 tn, but profitability has not scaled at the same pace.

Valuation at Current Share Price (~¥1,678, August 2025):

PER: ~2.9x FY2024 EPS (¥569.4), markedly lower than historical levels.

PBR: ~0.37x, well below 1.0x, indicating the market prices the company below its book value.

Dividend Yield: ~8.6%, an unusually high level relative to peers.

These metrics suggest that the market is applying a substantial discount to the company’s earnings and assets. While this could be interpreted as undervaluation, it may also reflect investor caution over:

the sustainability of current profit levels, particularly given U.S. housing headwinds;

exposure to FX and commodity volatility;

and a structural decline in ROE.

Investment Viewpoint:

Sumitomo Forestry represents a complex case. On one hand, the company combines cyclical housing exposure with long-term ESG drivers such as forest carbon credits and renewable energy, offering differentiated growth potential. On the other, the sharp discount in valuation multiples highlights market skepticism about the durability of earnings and efficiency of capital deployment.

Overall Assessment:

At current levels, the shares present a balance of opportunities and risks. For long-term investors, the key questions are whether Sumitomo Forestry can:

Sustain net income consistently above ¥100 bn,

Deliver on its mid-term targets of ¥3 tn revenue and ¥350 bn recurring profit by FY2027, and

Translate ESG initiatives into measurable returns.

The answers to these questions will determine whether today’s valuation reflects mispricing or a justified risk adjustment.

At Wasabi Info, we publish concise equity reports and market insights through our blog, and also provide custom, tailor-made research to support strategic decision-making for both private investors and corporations.

Our research services include:

• Equities: In-depth analysis of Japan-listed companies not featured in the blog

• Competitor Analysis: Detailed mapping of industry rivals and market dynamics

• Market Entry Intelligence: Insights into local barriers, regulations, and competitor positioning

• Real Estate & Assets: Localized assessments for factory, hotel, or retail expansion

• Field Intelligence: On-the-ground surveys and discreet market checks unavailable through public sources

Reports are available in English, Chinese, and Japanese.

For inquiries, please contact: admin@wasabi-info.com

© Wasabi Info | Privacy Policy

Disclaimer

This report is provided for informational purposes only and does not constitute investment, legal, or tax advice.

The analysis may include forward-looking statements and interpretations based on publicly available information as of the date of writing.

Readers are solely responsible for their own investment decisions and should seek advice from a licensed financial advisor or other qualified professional.

Wasabi-Info.com makes no representation or warranty, express or implied, regarding the accuracy, completeness, or reliability of the information contained herein, and shall not be held liable for any loss or damage arising from the use of this report.