Daiichi Sankyo Co., Ltd. (TSE: 4568): Stock Analysis

August 5, 2025

1. Introduction

Daiichi Sankyo Co., Ltd. (TSE: 4568) has been a major focus of investor attention over the past year due to its high-profile antibody-drug conjugate (ADC) pipeline and strong revenue growth. However, despite promising clinical progress and steady top-line expansion, the company’s share price has experienced a sharp correction.

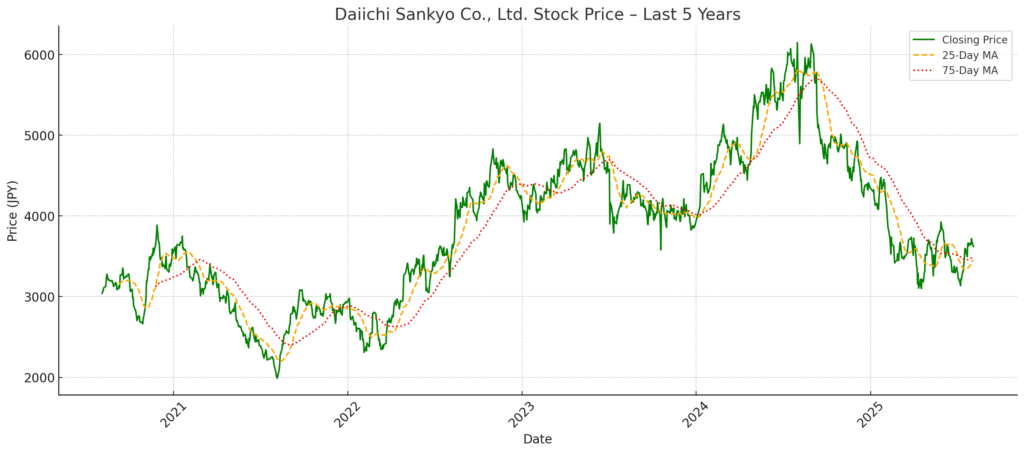

After reaching a peak of ¥6,131 on August 29, 2024, Daiichi Sankyo’s stock has declined by approximately 40%, trading at ¥3,620 as of August 4, 2025. This substantial downturn has raised questions among investors about the disconnect between the company’s strategic narrative and its financial performance.

This report explores the underlying causes of Daiichi Sankyo’s sharp share price decline. It examines a combination of operational and structural challenges—including profit margin compression, delayed R&D monetization, weakening capital efficiency, and a conservative approach to shareholder returns—to explain the shift in investor sentiment despite strong revenue and earnings growth.

2. Stock Price Overview

Peak Price: ¥6,131 on August 29, 2024

Current Price: ¥3,620 as of August 4, 2025

Decline from Peak: –40.9%

The stock price nearly halved over a span of 11 months despite strong top-line growth. This decline reflects not just market volatility but also deeper concerns about earnings quality, return on capital, and capital allocation. The company’s high valuation in 2024 was built on optimism around its oncology pipeline, particularly Enhertu and Dato-DXd. As monetization and margin visibility lagged, investor sentiment shifted decisively.

3. Financial and Operational Performance (FY2021–FY2025)

Daiichi Sankyo posted impressive revenue growth over the last five years:

| Fiscal Year | Revenue (¥ mn) | Operating Profit | Net Income | EPS (¥) | Dividend (¥) |

|---|---|---|---|---|---|

| FY2021 | 962,516 | 63,795 | 75,958 | 39.2 | 27 |

| FY2022 | 1,044,892 | 73,025 | 66,972 | 34.9 | 27 |

| FY2023 | 1,278,478 | 120,580 | 109,188 | 57.0 | 30 |

| FY2024 | 1,601,688 | 211,588 | 200,731 | 104.7 | 50 |

| FY2025 | 1,886,256 | 331,925 | 295,756 | 156.0 | 60 |

Key Highlights:

Revenue nearly doubled over five years (+96%).

Operating profit grew more than 5x from FY2021 to FY2025.

EPS grew nearly 4x, indicating significant per-share profitability growth.

However, this impressive performance failed to support the share price, largely due to concerns about sustainability, margin quality, and return on invested capital.

4. Key Drivers of Stock Price Decline

4.1 Margin and Earnings Pressure

What happened: Despite revenue and EPS growth, concerns linger around margin scalability and sustainability.

Investor concern: Will this growth be maintained? Is it profitable growth?

Root causes:

Enhertu’s margin contribution is constrained by the AstraZeneca profit-sharing model.

Growing SG&A costs tied to commercialization of new ADCs.

Increasing manufacturing and quality control costs for ADC production.

Summary: Although earnings rose, margins remained structurally limited—leading investors to reassess profitability potential.

4.2 R&D Burden and Monetization Lag

What happened: R&D intensity exceeded 20% of revenue in recent years.

Investor concern: When will this massive R&D investment translate into cash flow?

Root causes:

Multiple late-stage ADC programs in parallel (Enhertu, Dato-DXd, DS-3939, DS-7300).

Large-scale CapEx for ADC manufacturing capacity.

Regulatory timelines and market uptake remain uncertain for many candidates.

Summary: Investors are concerned that the payoff from this high R&D burden is not yet visible, and returns may be lower than expected due to cost-sharing and delayed approvals.

4.3 Declining Capital Efficiency

What happened: ROE remained in the low single digits even in FY2025.

Investor concern: Is capital being effectively deployed?

Root causes:

Profit growth trails behind capital reinvestment.

No offsetting capital actions (e.g., buybacks) to support ROE or EPS.

Accumulating equity dilutes return metrics.

Summary: Despite rising earnings, returns on capital are not improving proportionately, leading to valuation compression.

4.4 Conservative Shareholder Returns

What happened: Dividends rose modestly (from ¥27 to ¥60), but yield remains under 2%.

Investor concern: Capital allocation is overly conservative.

Root causes:

Management prioritizes reinvestment over payouts.

No buybacks or special dividends announced, even at peak valuation.

Dividend policy lags global pharma peers.

Summary: Lack of aggressive return policies makes the stock less appealing, especially as growth enters a normalization phase.

5. Strategic Outlook and Catalysts

5.1 Strategic Outlook

Daiichi Sankyo remains strategically positioned as a global leader in Antibody-Drug Conjugate (ADC) innovation. Its long-term vision revolves around transforming into a “Global Oncology Top-Tier Company” by 2030, leveraging its proprietary DXd technology and expanding its presence in high-growth international markets.

Key Strategic Pillars:

Oncology Leadership via ADCs

Enhertu (DS-8201): Commercial success in breast, gastric, and lung cancers.

Dato-DXd: Potential next blockbuster targeting non-small cell lung cancer (NSCLC).

DS-3939, DS-7300, and DS-6000: In advanced development phases.

Geographic Expansion

Strengthening sales and regulatory functions in the U.S., EU, and China.

Building out oncology-focused commercial infrastructure, especially in North America.

Manufacturing Excellence for ADCs

Continued capital investment in Japan and the U.S. to build scalable, high-quality ADC production capacity.

Digital Transformation (DX)

Ongoing initiatives in drug discovery, clinical trial management, and supply chain optimization using AI and data science.

Strategic Risk Management: The company has reduced reliance on traditional cardiovascular and generic segments and is streamlining operations to focus resources on oncology innovation.

5.2 Near-to-Mid-Term Catalysts

| Catalyst | Description | Timeline | Potential Impact |

|---|---|---|---|

| Dato-DXd Phase 3 Results | Readouts from pivotal trials in NSCLC and breast cancer. | FY2025–2026 | High – May validate next ADC franchise |

| Enhertu Label Expansion | Regulatory approvals for additional indications (e.g., early-stage cancers). | Ongoing | Moderate to High |

| China Market Entry | Progress in Enhertu launch in China (in partnership with AstraZeneca). | FY2025–2027 | High – New revenue pool |

| ADC Manufacturing Ramp-Up | Completion of new facilities to support global ADC demand. | FY2026–2027 | Moderate – Supports scalability |

| Strategic Partnerships | Possible new co-development/licensing deals leveraging DXd platform. | Opportunistic | Moderate |

| Shareholder Return Policy Shift | Potential increase in dividend payout ratio or introduction of buybacks. | FY2025–2026? | High (if executed) |

Investor Watchpoint: Positive clinical data and accelerated regulatory decisions could significantly re-rate the stock. However, delays or negative trial outcomes would weigh heavily due to high pipeline concentration.

6. Risks

While Daiichi Sankyo offers compelling long-term growth potential through its ADC pipeline, several risks—both structural and near-term—must be considered by investors.

6.1 Pipeline Concentration and Clinical Risk

Description:

The company’s medium- to long-term growth is heavily dependent on the success of a small number of ADC assets, particularly Enhertu and Dato-DXd.

Implications:

Clinical trial failure or safety concerns could materially impair growth expectations.

High expectations for Dato-DXd set a low tolerance for any delays or negative outcomes.

Heavy R&D allocation to ADCs limits diversification across therapeutic areas.

This is the single most significant source of downside risk in valuation models.

6.2 Profit-Sharing and Limited Margin Leverage

Description:

The co-development agreement with AstraZeneca for Enhertu significantly limits Daiichi Sankyo’s ability to scale earnings in proportion to global sales.

Implications:

Enhertu’s commercial success benefits AstraZeneca more than Daiichi Sankyo on a per-unit basis.

Milestone-driven revenue creates volatility in reported earnings.

Margin expansion is structurally constrained, even under optimistic sales scenarios.

This reduces the earnings leverage typically associated with blockbuster drugs.

6.3 Manufacturing Complexity and Capacity Risk

Description:

ADCs require highly specialized manufacturing processes, with limited redundancy and significant upfront capital investment.

Implications:

Delays in plant construction or validation could disrupt supply.

Quality control issues would carry high reputational and financial cost.

Cost of goods sold (COGS) is relatively high, impacting gross margins.

6.4 Regulatory and Pricing Pressures

Description:

As Daiichi Sankyo globalizes its oncology business, it faces increasingly diverse regulatory and reimbursement environments.

Implications:

Approval delays or additional safety data requests may affect launch timelines.

Pricing pressures in the U.S., EU, and China could reduce profitability.

ADCs, being high-cost therapies, may be subject to stricter cost-benefit scrutiny by payers.

6.5 Capital Allocation and Shareholder Return Policies

Description:

The company maintains a conservative dividend and has not implemented share buybacks, despite a strong balance sheet.

Implications:

Missed opportunity to support EPS and valuation via capital actions.

Continued conservatism may deter income-focused or value-oriented investors.

Misalignment between management’s long-term focus and market’s shorter-term expectations.

6.6 Competitive Landscape in Oncology

Description:

The oncology space is rapidly evolving, with several global players developing competing ADC platforms (e.g., Seagen, Pfizer, Roche, ImmunoGen).

Implications:

Daiichi Sankyo must maintain a first-mover advantage through clinical superiority and speed.

Potential pricing wars or loss of exclusivity (LOE) could compress margins.

Collaborators like AstraZeneca may prioritize other pipeline products if ROI expectations shift.

Summary Table: Risk Profile

| Category | Risk Summary | Impact | Probability |

|---|---|---|---|

| Pipeline Dependence | Heavy reliance on a few ADC assets | Very High | Medium |

| Profit-Sharing Constraints | Limits margin scalability for Enhertu | High | High |

| Manufacturing Risk | Complex and capital-intensive ADC production | Moderate | Medium |

| Regulatory/Pricing Pressure | Global access and reimbursement risks | Moderate | Medium–High |

| Shareholder Return Policy | Conservative capital allocation | Moderate | High |

| Competitive Pressure | Innovation race in ADC and oncology | Moderate | Medium |

7. Conclusion

Daiichi Sankyo stands at a critical juncture. Over the past five years, the company has demonstrated robust revenue and earnings growth, driven by its transformation into a global oncology innovator. Its antibody-drug conjugate (ADC) portfolio, particularly Enhertu and Dato-DXd, holds blockbuster potential and has already begun reshaping its revenue base.

However, the market has significantly repriced the stock—down nearly 40% from its August 2024 peak—despite this growth. This divergence reflects growing investor concerns over margin limitations, delayed R&D monetization, shareholder return policies, and execution risks tied to manufacturing and clinical development.

Key Takeaways:

The company’s long-term growth narrative remains intact, but its near-term valuation is under pressure due to structural and strategic frictions.

Valuation has corrected to more reasonable levels (~23x PER), providing a potential entry point for long-term investors if key catalysts (e.g., Dato-DXd Phase 3 data) materialize positively.

The stock’s re-rating will depend not only on clinical success, but also on improved capital efficiency and more investor-aligned return strategies.

At Wasabi Info, we publish concise equity reports and market insights through our blog—

but our core value lies in providing bespoke, on-demand research for international clients.

Whether you are a private investor or a corporation, we deliver confidential, tailored intelligence designed to support strategic decisions.

Our research services include:

• Equities: In-depth analysis of Japan-listed companies not featured in the blog

• Competitor Analysis: Detailed mapping of industry rivals and market dynamics

• Market Entry Intelligence: Insights into local barriers, regulations, and competitor positioning

• Real Estate & Assets: Localized assessments for factory, hotel, or retail expansion

• Field Intelligence: On-the-ground surveys and discreet market checks unavailable through public sources

Reports are available in English, Chinese, and Japanese.

For inquiries, please contact: admin@wasabi-info.com

© Wasabi Info | Privacy Policy

Disclaimer

This report is intended for informational purposes only and does not constitute investment advice. The analysis contains forward-looking statements and interpretations based on publicly available information as of the date of writing. Readers should conduct their own research and consult with a licensed financial advisor before making any investment decisions.

Wasabi-Info.com shall not be held liable for any loss or damage arising from the use of this report or reliance on its contents.