Mitsubishi Heavy Industries, Ltd. (TSE: 7011): Stock Analysis

August 7, 2025

1. Introduction: From Legacy Giant to Market Surprise

Once perceived as a traditional heavy machinery conglomerate tethered to Japan’s postwar industrial past, Mitsubishi Heavy Industries (MHI) has undergone a remarkable revaluation in the eyes of global investors. Over the past two years, the company’s stock price has surged by approximately 500%, transforming MHI from a stable but unexciting industrial stalwart into one of the most compelling turnaround stories in Asia’s equity markets.

This dramatic shift has caught the attention of both institutional and retail investors, many of whom are now asking the same question:

What’s driving Mitsubishi Heavy Industries’ meteoric rise — and can it continue?

Unlike many short-lived rallies sparked by speculation, MHI’s ascent appears deeply rooted in structural improvements across its business segments. The company has achieved record-level profitability, strengthened its balance sheet, and repositioned its portfolio to align with Japan’s defense expansion, global decarbonization trends, and smart infrastructure development.

At the same time, its evolving strategic direction — guided by a disciplined medium-term management plan — has fueled growing confidence in the company’s long-term growth trajectory. As a result, MHI now stands at a critical intersection of macroeconomic tailwinds, geopolitical relevance, and internal transformation.

This report takes a closer look at how MHI reached this pivotal point. We will analyze the timeline of its stock price development, examine key financial metrics, break down the catalysts behind the rally, and evaluate whether its current momentum is sustainable. For investors seeking exposure to Japan’s industrial resurgence, MHI offers a case worth examining in detail.

2. Stock Price Development: A Remarkable Two-Year Climb

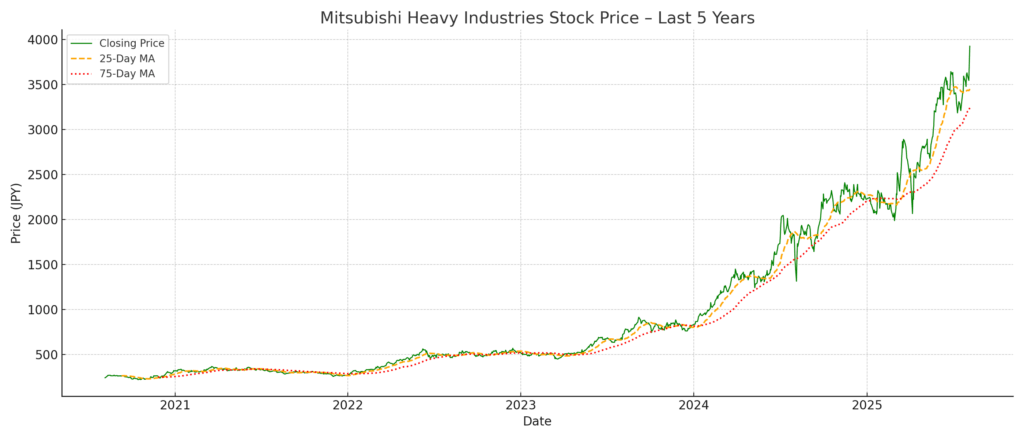

MHI’s share price has undergone a dramatic transformation since mid-2023. Trading at around ¥670 per share in June 2023, the stock has climbed to over ¥3,900 by August 2025 — a rally of nearly 500%. While Japanese equities broadly benefited from a favorable macro backdrop during this period, MHI’s rise was significantly sharper and more sustained than most of its industrial peers.

Timeline of Key Price Movements

| Date | Approx. Price (JPY) | Key Event / Market Context |

|---|---|---|

| Jun 2023 | ~¥670 | Pre-rally baseline; muted investor interest |

| Oct 2023 | ~¥830 | Momentum builds amid strong Q2 earnings |

| Jan 2024 | ~¥820 | Defense-related speculation begins |

| Apr 2024 | ~¥1,380 | FY2023 results exceed expectations |

| Oct 2024 | ~¥2,280 | FY2024 outlook revised upward |

| Aug 2025 | ~¥3,930 | Fivefold increase from 2023 levels |

This upward trajectory has significantly outpaced the Nikkei 225 and TOPIX indices, signaling that MHI’s performance is driven by more than macroeconomic tailwinds. The company’s stock price appreciation reflects a combination of fundamental earnings growth, strategic repositioning, and a broader market re-rating of Japan’s industrial base.

Changing Investor Perception

Prior to this rally, MHI was often viewed as a legacy conglomerate — burdened by slow-moving business segments, underperforming assets, and project execution challenges. However, the market narrative began to shift in late 2023, as several critical developments unfolded:

Operating profits and EPS began to recover, reaching record highs by FY2024.

The company adopted a more focused strategy aligned with global themes: defense, decarbonization, and smart infrastructure.

MHI demonstrated strong financial discipline, including reduced debt and improved return on equity.

Japan’s domestic policy environment turned favorable for defense and green energy spending — both core areas for MHI.

These factors gradually transformed investor sentiment. From being a deep-value play with little growth visibility, MHI evolved into a structural growth story — with a re-rating that reflected confidence in long-term earnings power.

3. Financial Performance: A Five-Year Turnaround Story

Over the past five fiscal years, MHI has undergone a significant financial transformation, turning from a low-margin industrial conglomerate into a high-performing enterprise with improving profitability, balance sheet strength, and capital efficiency. The company’s resurgence is not a product of a single catalyst, but rather the result of strategic restructuring, cost control, and operating leverage driven by growth in key segments such as defense and energy systems.

Key Financial Metrics (FY2021–FY2025)

| Fiscal Year End | Revenue (JPY bn) | Operating Profit (JPY bn) | Net Income (JPY bn) | EPS (JPY) | Dividend (JPY) |

|---|---|---|---|---|---|

| FY2021 (Mar-21) | 3,700 | 54.1 | 40.6 | 12.1 | 7.5 |

| FY2022 (Mar-22) | 3,860 | 160.2 | 113.5 | 33.8 | 10 |

| FY2023 (Mar-23) | 4,203 | 193.3 | 130.5 | 38.8 | 13 |

| FY2024 (Mar-24) | 4,657 | 282.5 | 222.0 | 66.1 | 20 |

| FY2025 (Mar-25) | 5,027 | 383.2 | 245.4 | 73.0 | 23 |

Performance Highlights

Revenue Growth:

MHI’s top line has expanded at a 5-year CAGR of ~7.9%, driven by strong demand in Energy Systems (gas turbines, hydrogen/ammonia solutions), Defense & Space, and Smart Infrastructure.Profitability Surge:

Operating margin improved from 1.5% in FY2021 to 7.6% in FY2025, reflecting disciplined cost control, improved project execution, and a favorable business mix.Net Income & EPS:

Net profit increased sixfold, with EPS rising from ¥12.1 to ¥73.0, supported by robust after-tax margins and the absence of major impairment charges.Capital Efficiency:

ROE has recovered to double-digit levels, aided by improved asset turnover and profit margins. The equity ratio remained above 30%, providing financial flexibility.Shareholder Returns:

Dividends have been steadily increased from ¥7.5/share (FY2021) to ¥23/share (FY2025), and the company maintains a Dividend-on-Equity (DOE) policy to ensure payout consistency.

The numbers tell a compelling story of financial normalization and structural growth. Rather than relying on short-term cost cuts or one-off gains, MHI’s performance improvements stem from underlying operational strength — particularly in businesses aligned with long-term megatrends such as decarbonization, national security, and digital infrastructure.

4. Drivers of Stock Price Appreciation

The near fivefold increase in MHI’s share price from mid-2023 to mid-2025 was not driven by speculative momentum. Rather, it was the result of a convergence of long-term structural forces, a clear shift in strategic direction, and an evolving investor appreciation for the company’s role in national security, energy transition, and industrial resilience.

What follows is a breakdown of the key factors that underpinned this dramatic revaluation.

1. Defense Segment Transformation and Geopolitical Tailwinds

One of the most impactful growth drivers was MHI’s transformation into a central pillar of Japan’s defense industrial base.

Massive Defense Orders: The Japanese government’s official shift to increase defense spending to 2% of GDP (NATO standard) by FY2027 directly benefited MHI, which manufactures submarines, fighter jets, missile systems, and launch vehicles. Order backlogs in defense and space surged as a result.

Global Security Context: Heightened geopolitical tensions in East Asia further bolstered investor interest in MHI as a national security proxy.

Impact on valuation: The defense business, previously seen as low-margin and politically constrained, was re-rated as a growth engine with recurring revenue and high barriers to entry.

2. Decarbonization Megatrends and Energy Solutions

MHI capitalized on the global push for decarbonization by expanding its offerings in hydrogen, ammonia, and carbon capture:

Energy Systems Leadership: MHI ramped up commercial deployment of hydrogen-ready gas turbines and CO₂ capture technologies, gaining early-mover advantage.

Ammonia Combustion Projects: The company advanced demonstration projects for ammonia-fueled power generation — a key area in Japan’s energy transition roadmap.

Investor perception shift: MHI was increasingly viewed not as a “brown” energy player but as a transition-critical infrastructure company positioned to benefit from green subsidies and international cooperation.

3. Smart Infrastructure and Global Engineering Resurgence

The Smart Infrastructure and Plant/Engineering divisions also played a key role:

Urban systems and digital energy (including distributed power, building automation, and HVAC solutions) grew steadily, offering margin stability.

Engineering services recovered, benefiting from disciplined project selection and global industrial investment cycles.

Combined with ongoing digitalization, this created an appealing growth and margin profile in previously underperforming segments.

4. Medium-Term Business Plan Credibility

MHI’s 2024–2026 Medium-Term Business Plan, released in May 2023, provided a clear roadmap for growth and capital discipline:

Targeted ¥5 trillion in revenue and ¥400 billion in operating profit by FY2025 — both of which were effectively achieved a year ahead of schedule.

ROIC and ROE targets introduced investor-relevant KPIs

Emphasis on capital efficiency and return to shareholders reinforced investor confidence

Result: The plan served as an anchor for re-rating — especially as execution consistently exceeded guidance.

5. Stronger Financial Discipline and Shareholder Returns

MHI’s stock was historically discounted due to concerns about poor capital allocation and legacy liabilities. From FY2021 onward, the company addressed these through:

Free cash flow generation and net debt reduction

Increased dividends and steady DOE-based return policy

No major impairment losses or balance sheet shocks

This financial normalization — especially against a backdrop of structural growth — helped attract foreign institutional investors.

6. Investor Re-rating of Japanese Industrial Champions

Finally, MHI’s revaluation coincided with a broader rotation into Japanese equities, particularly those with:

Underutilized assets

Global growth alignment

Domestic political support

MHI fit this profile exceptionally well — bridging deep industrial heritage with next-generation relevance.

5. MHI’s Strategy and Mid-Term Plan (FY2024–FY2026)

MHI’s recent stock revaluation has been anchored by a bold and well-received Medium-Term Business Plan, covering FY2024 to FY2026. The plan is centered on reinforcing profitability, capturing megatrends, and shifting capital allocation toward growth and innovation. It also marks a transition from post-restructuring stabilization to offensive investment and value creation.

Strategic Framework

The plan is built on three core strategic pillars:

Strengthening Business Portfolio Resilience

Focusing resources on businesses with global competitiveness and high capital efficiency

Downsizing or exiting low-return, non-core operations

Enhancing margin structure in core divisions: Energy Systems, Defense & Space, Smart Infrastructure

Creating Growth Engines for the Next Decade

Driving commercialization of CO₂ capture, hydrogen/ammonia combustion, and small-scale nuclear (SMRs)

Scaling up digital solutions and smart city infrastructure

Strengthening defense capability to align with Japan’s national strategy

Improving Corporate Value and Capital Efficiency

Targeting ROE of 10% and ROIC of 8%

Committing to stable shareholder returns via DOE-linked dividends

Enhancing sustainability practices and ESG disclosure

Quantitative Targets (FY2025 Plan-End)

| Metric | Target by FY2025 | Status as of FY2024 Actual |

|---|---|---|

| Revenue | ¥5 trillion | ¥4.66 trillion |

| Operating Profit | ¥400 billion | ¥282.5 billion |

| Operating Margin | 8% | 6.1% |

| ROE | ≥10% | 8.6% |

| Net Debt-to-Equity Ratio | ~0.5x | Achieved ahead of schedule |

| Dividend (DOE-linked) | Sustainable growth | Increased to ¥20/share |

MHI is already ahead of schedule on multiple fronts — particularly in revenue and capital structure improvements

Segment Strategies

1. Energy Systems

Expand delivery of hydrogen-ready gas turbines

Advance ammonia-fired boilers and CO₂ capture (CCUS) systems

Build partnerships in global energy transition infrastructure

2. Defense & Space

Scale up production of submarines, missile systems, and space launch vehicles

Actively participate in Japan’s multi-year defense modernization

Increase internal capacity and vertical integration to meet rising demand

3. Smart Infrastructure / Industrial Systems

Promote distributed energy, mobility infrastructure, and factory automation

Introduce “Energy-as-a-Service” and predictive maintenance models

Leverage AI/IoT for systems integration and smart city solutions

Capital Allocation and Investment Discipline

Over the plan period, MHI intends to invest approximately ¥1.2 trillion, allocated as follows:

55% for growth investments (including decarbonization tech and digital solutions)

30% for maintenance and productivity enhancement

15% for strategic M&A and technology alliances

Management emphasizes a selective and returns-focused approach, with strict hurdle rates based on business segment profitability and market positioning

Progress and Market Confidence

By FY2025 Q1, MHI had already made significant headway:

Order intake in defense and energy exceeded forecasts

Profit margins improved across most business units

Shareholder returns were raised, reflecting earnings visibility and FCF stability

Investor confidence has strengthened not just in the financial targets, but in the company’s ability to execute a credible transformation — making the plan one of the central justifications for the stock’s re-rating.

6. Catalysts and Risks

MHI stands at the intersection of powerful secular growth drivers and complex execution challenges. While the company’s medium-term plan outlines a credible and transformative growth trajectory, its future performance will be shaped by both positive catalysts and material risks. Below is an overview of each.

6.1 Catalysts

1. Expansion of Defense Orders

Continued increases in Japan’s defense budget (toward 2% of GDP by FY2027) will directly benefit MHI as a primary contractor for submarines, missile systems, and fighter jets.

Acceleration of exports and joint defense development (e.g., GCAP with the UK and Italy) could open international revenue streams

2. Global Energy Transition Tailwinds

Full-scale commercialization of hydrogen, ammonia, and carbon capture technologies may unlock new growth markets and subsidized projects.

Rising energy security concerns in Europe and Asia favor domestic suppliers of large-scale power solutions — MHI is positioned to lead.

3. Smart Infrastructure and Digitalization

Demand for energy-efficient, connected urban infrastructure is increasing.

MHI’s “Energy-as-a-Service” and factory automation platforms could benefit from smart city and Industry 4.0 investment cycles.

4. Structural Investor Tailwind in Japan

Japan’s capital market reform and push for higher ROE (via TSE Prime pressure) continues to attract foreign inflows.

MHI, now ROE-focused and dividend-growing, is aligned with this narrative.

5. Shareholder Return Upside

If free cash flow continues to improve, dividend increases and potential buybacks could support further valuation re-rating.

6.2 Risks

1. Execution Risk in New Technologies

While MHI is pioneering hydrogen turbines, SMRs, and CCUS, these remain pre-profit or demonstration-stage technologies.

Cost overruns, technological hurdles, or delays could impair capital efficiency and investor confidence.

2. Exposure to Global Supply Chains

High dependence on precision components and materials (especially in defense and energy systems) creates vulnerability to geopolitical shocks and inflation in input costs.

3. Capital Allocation and M&A Discipline

Aggressive investment (¥1.2 trillion over 3 years) raises the risk of misallocation, especially in new growth areas.

Failure to meet ROI targets could reverse investor goodwill.

4. Geopolitical Uncertainties

While defense demand is rising, regional conflict escalation or diplomatic shifts (e.g., export restrictions) could impact long-term order visibility.

MHI’s dual exposure to both Western and East Asian markets adds strategic complexity.

5. Dependence on Government Policy

MHI’s momentum in defense and green energy is policy-dependent. Any reversal in subsidies, procurement plans, or energy targets would be materially negative.

6. Talent and Organizational Challenge

Expanding high-tech businesses and executing multiple strategic fronts requires rapid upskilling, which may strain organizational capacity in the short term.

7. Conclusion

MHI has undergone a profound transformation over the past two years — not only in terms of its share price performance, but also in how the company is positioned within Japan’s industrial and strategic framework.

Once seen as a slow-moving industrial conglomerate, MHI is now viewed as a critical player in national defense, a technological enabler of the energy transition, and a key platform provider for smart infrastructure. Its Medium-Term Business Plan (FY2024–2026) has been instrumental in reshaping investor perceptions, with clear strategic focus, ambitious yet achievable targets, and visible execution discipline.

While the stock’s nearly fivefold rise between mid-2023 and mid-2025 may raise concerns about overheating, MHI’s valuation is now more reflective of its long-term earnings power and strategic relevance — particularly in a world where industrial self-sufficiency, energy security, and defense readiness are paramount.

Going forward, sustained value creation will depend on:

Continued execution of high-tech growth initiatives (hydrogen, CCUS, SMRs)

Resilience in navigating geopolitical and supply chain volatility

Shareholder alignment through disciplined capital returns

In short, MHI’s story is no longer just about cyclical recovery or restructuring. It is about strategic ascendancy in a rapidly changing global environment — and investors are beginning to price in that structural shift.

At Wasabi Info, we publish concise equity reports and market insights through our blog—

but our core value lies in providing bespoke, on-demand research for international clients.

Whether you are a private investor or a corporation, we deliver confidential, tailored intelligence designed to support strategic decisions.

Our research services include:

• Equities: In-depth analysis of Japan-listed companies not featured in the blog

• Competitor Analysis: Detailed mapping of industry rivals and market dynamics

• Market Entry Intelligence: Insights into local barriers, regulations, and competitor positioning

• Real Estate & Assets: Localized assessments for factory, hotel, or retail expansion

• Field Intelligence: On-the-ground surveys and discreet market checks unavailable through public sources

Reports are available in English, Chinese, and Japanese.

For inquiries, please contact: admin@wasabi-info.com

© Wasabi Info | Privacy Policy

Disclaimer

This report is intended for informational purposes only and does not constitute investment advice. The analysis contains forward-looking statements and interpretations based on publicly available information as of the date of writing. Readers should conduct their own research and consult with a licensed financial advisor before making any investment decisions.

Wasabi-Info.com shall not be held liable for any loss or damage arising from the use of this report or reliance on its contents.