Central Japan Railway Company (TSE: 9022): Stock Analysis

August 10, 2025

1. Introduction

Central Japan Railway Company (JR Central) operates the Tokaido Shinkansen and a network of conventional lines across central Japan, serving as a vital link between Tokyo, Nagoya, and Osaka. The company’s business model is heavily reliant on passenger transportation, complemented by real estate, retail, and other ancillary operations. Post-pandemic, JR Central has undergone a robust recovery, benefiting from the resurgence in domestic travel, inbound tourism, and structural demand from business commuters.

In recent years, JR Central has also intensified capital investments in the Chuo Shinkansen maglev project, safety upgrades, and station redevelopment, while managing the post-COVID balance sheet normalization. The 2025 World Expo in Osaka and continued inbound tourism growth provide supportive demand tailwinds.

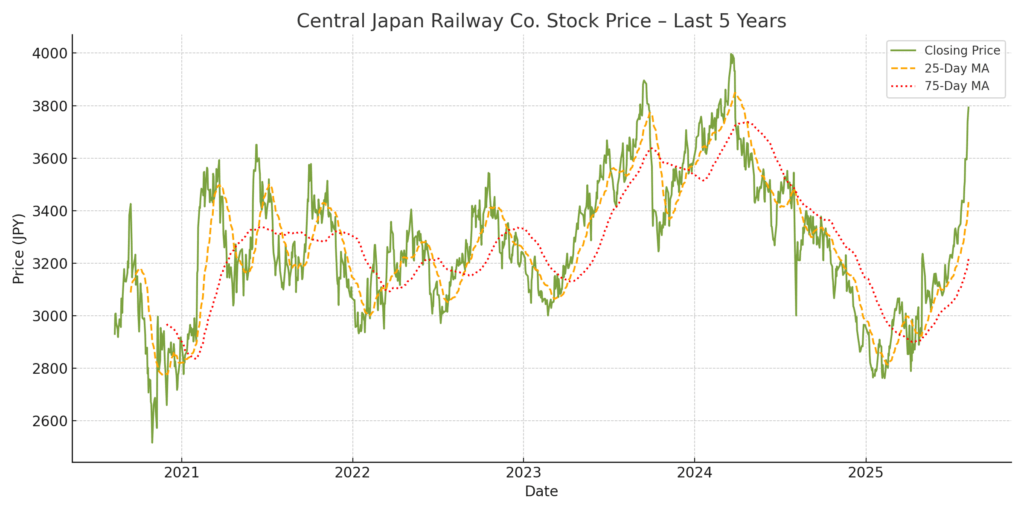

2. Stock Price Development

Over the past five years, JR Central’s share price has exhibited pronounced cyclicality:

2020–2022: Pandemic-induced collapse in passenger volumes triggered significant earnings losses and a steep share price decline.

2022–2023: Gradual recovery began with the lifting of travel restrictions and resumption of Shinkansen demand.

2023–2025: Strong rebound driven by restored profitability, surging inbound tourism, and cost control efforts. By mid-2025, the stock traded near multi-year highs, reflecting restored investor confidence.

Price momentum has also been supported by a consistent dividend policy, albeit with modest increases from ¥26 in FY2021–FY2022 to ¥31 in FY2025.

3. Financial and Operational Analysis

3.1 Key Financial Metrics (Unit: million yen, EPS/Dividend in yen)

| Fiscal Year | Revenue | Operating Profit | Ordinary Profit | Net Profit | EPS | DPS |

|---|---|---|---|---|---|---|

| FY2021 | 823,517 | -184,751 | -262,064 | -201,554 | -205.1 | 26 |

| FY2022 | 935,139 | 1,708 | -67,299 | -51,928 | -52.8 | 26 |

| FY2023 | 1,400,285 | 374,503 | 307,485 | 219,417 | 223.0 | 27 |

| FY2024 | 1,710,407 | 607,381 | 546,946 | 384,411 | 390.7 | 29 |

| FY2025 | 1,831,847 | 702,794 | 649,294 | 458,423 | 465.9 | 31 |

3.2 Observations

Strong post-pandemic rebound: Revenue more than doubled from FY2021 to FY2025, reflecting recovery in Shinkansen demand and regional travel.

Operating leverage: Return to profitability in FY2022 was muted, but rapid margin expansion followed in FY2023–FY2025 as fixed costs were absorbed by higher volumes.

Margin profile: FY2025 operating margin exceeded 38%, highlighting the high fixed-cost nature of rail operations once capacity utilization normalizes.

Dividend policy: Conservative yet stable, with gradual DPS increases. Payout ratio remains modest given large-scale capex needs.

Balance sheet: Ongoing heavy investment in Chuo Shinkansen and infrastructure renewal has kept net debt elevated, though operating cash flows have strengthened.

4. Chuo Shinkansen (Maglev) Project – Financial Impact and Future Outlook

Project Overview

The Chuo Shinkansen is JR Central’s flagship long-term investment, deploying superconducting maglev technology to connect Tokyo and Nagoya in approximately 40 minutes, with an eventual extension to Osaka. The Tokyo–Nagoya segment was originally targeted for 2027 but is now delayed due to construction and environmental approval issues in Shizuoka Prefecture .

Capital Investment Scale and Financial Impact

Total projected investment for the Tokyo–Nagoya segment is estimated at ~¥7 trillion, with JR Central funding the project predominantly through long-term debt and operating cash flows .

Annual capital expenditure on the maglev has ranged between ¥400–500 billion in recent years, representing the single largest component of JR Central’s investment program .

The heavy front-loaded capex has kept free cash flow under pressure, limiting dividend growth despite strong operating profits from the Tokaido Shinkansen.

Debt ratios are expected to remain elevated until after the commencement of operations.

Revenue Potential Post-Opening

Initial operational forecasts suggest annual ridership of around 86,000 passengers per day for Tokyo–Nagoya, with fare revenues potentially exceeding ¥300–400 billion per year once stabilized .

The maglev is expected to capture high-yield business travel demand and potentially shift some traffic from air travel on the Tokyo–Nagoya–Osaka corridor.

Beyond direct ticket revenue, station-area development and ancillary commercial opportunities could add incremental income.

Impact on Existing Tokaido Shinkansen

The Tokaido Shinkansen will continue to operate alongside the maglev, but its role will shift:

For Tokyo–Nagoya–Osaka travel, the maglev will target high-speed, premium demand, while the Tokaido line will focus on intermediate stops and price-sensitive segments .

This dual operation is expected to optimize network utilization and maintain resilience in case of disruptions on either line.

Management does not foresee decommissioning significant Tokaido capacity in the short to medium term; instead, service frequency adjustments may be implemented to match evolving demand.

Strategic Considerations

The Chuo Shinkansen reinforces JR Central’s technological leadership and offers long-term growth potential beyond the limits of the Tokaido line’s capacity.

However, the project carries execution, regulatory, and financing risks, with delays already impacting investor sentiment.

Successful completion and ramp-up could materially lift group revenue, but breakeven may take several years post-launch.

5. Strategic and Technological Positioning

5.1 Core Business Moat – Tokaido Shinkansen Monopoly

JR Central operates the Tokaido Shinkansen, Japan’s most critical high-speed rail artery, linking Tokyo, Nagoya, and Osaka. This corridor accounts for roughly 85% of JR Central’s transportation revenue and handles over 160 million passenger trips annually in normal demand conditions. The line’s strategic importance lies in:

Near-monopoly position: No competing high-speed rail services exist along the full route, and air travel is disadvantaged by longer door-to-door times and limited airport connectivity in central Tokyo and Osaka.

High frequency and reliability: Departures every few minutes at peak times, with punctuality averaging under one minute delay per train.

Business travel capture: Corporate commuter demand remains structurally high, particularly between Tokyo and Nagoya, making revenues relatively resilient even during economic slowdowns compared to leisure-oriented routes.

The scale, exclusivity, and embedded demand patterns form a deep competitive moat, enabling sustained pricing power and stable cash flows.

5.2 Technological Leadership – Chuo Shinkansen Maglev

The Chuo Shinkansen represents a transformational leap in high-speed rail, deploying superconducting maglev technology capable of operating at 500 km/h. Key strategic elements include:

World-first long-distance maglev: Positions JR Central as a global leader in advanced rail systems, potentially opening export opportunities.

Capacity relief for Tokaido line: The maglev will handle the fastest express services, freeing capacity on the Tokaido Shinkansen for regional and intermediate-stop demand.

Innovation ecosystem: The maglev project has driven advancements in tunnel engineering, energy efficiency, and environmental mitigation, which could have spillover benefits across JR Central’s broader operations.

While the project faces regulatory delays and high capex burdens, successful completion would cement JR Central’s reputation as a technological pioneer and create a second high-speed backbone for Japan’s transport network.

5.3 Real Estate and Retail Synergies

JR Central leverages its station footprint to generate stable non-fare revenue, accounting for roughly 10–15% of total operating income:

Flagship developments: JR Central Towers and JR Gate Tower in Nagoya integrate office, hotel, and retail spaces, producing recurring rental and service revenue.

Transit-oriented commercial hubs: Station-adjacent malls, convenience stores, and dining facilities capture high passenger foot traffic.

Event-driven demand: Large-scale events (e.g., 2025 Osaka Expo) can drive incremental retail and hospitality revenue.

The real estate strategy is defensive in downturns, as station traffic remains relatively stable compared to standalone retail assets, providing a counterbalance to transportation revenue volatility.

5.4 Operational Resilience

JR Central consistently ranks among the most reliable rail operators globally, supported by:

Safety systems: Continuous investment in earthquake detection, automatic train control, and infrastructure inspection technology minimizes accident risk.

Rolling stock renewal: Introduction of N700S Shinkansen sets improves energy efficiency, ride comfort, and maintenance intervals.

Digital transformation: Expanded use of e-ticketing (e.g., smart card and mobile reservations) enhances customer convenience and operational data analytics.

Disaster recovery protocols: Redundant systems and disaster training ensure rapid service restoration after seismic or weather-related disruptions.

These measures underpin brand trust, regulatory goodwill, and the ability to maintain operations under adverse conditions.

6. Risks and Catalysts

6.1 Catalysts

2025 Osaka World Expo: Expected to drive incremental travel demand.

Inbound tourism: Continued yen weakness and global travel recovery should sustain foreign visitor volumes.

Maglev progress: Resolution of regulatory hurdles in Shizuoka section could trigger re-rating.

Cost discipline: Further operational efficiency gains may support margin expansion.

6.2 Risks

Capex overhang: Chuo Shinkansen requires sustained multi-trillion-yen investment, potentially pressuring free cash flow.

Regulatory/environmental delays: Ongoing disputes over water resources in Shizuoka section risk pushing back project timelines.

Economic sensitivity: While commuter demand is stable, business travel could be vulnerable to economic slowdowns or remote work trends.

Natural disasters: Earthquakes or extreme weather could disrupt operations and infrastructure.

7. Conclusion

JR Central has successfully transitioned from pandemic-induced losses to record profitability within just four fiscal years, driven by the structural resilience of the Tokaido Shinkansen and disciplined cost management. The company is now entering a dual-phase growth narrative: sustaining strong earnings from its core high-speed rail franchise while progressing toward the transformative Chuo Shinkansen maglev project.

From an operational standpoint, the near-monopoly position in Japan’s busiest transport corridor continues to deliver stable and predictable cash flows, supported by premium business travel demand and high service reliability. Non-fare revenue streams from station real estate and retail operations provide additional earnings diversification.

On the strategic side, the maglev project represents a once-in-a-generation infrastructure investment that could significantly expand JR Central’s addressable market and reinforce its technological leadership. However, this comes with execution, regulatory, and financing risks—with capex overhang likely to limit free cash flow and dividend growth in the medium term.

Valuation Considerations

As of August 8, 2025, JR Central’s share price stands at ¥3,793, implying:

P/E (FY2025 EPS ¥465.9): ~8.1x

P/B: ~0.81x (based on FY2025 book value per share of ¥4,675)

Dividend yield: ~0.9% (FY2025 annual dividend ¥35)

At these levels, the stock trades below both its pre-pandemic average multiples and the broader Japanese transport sector, reflecting lingering concerns over maglev delays, capex burden, and macro uncertainty. This suggests a valuation discount relative to the company’s long-term earnings power.

Investment View

Base Case: At the current valuation, JR Central appears undervalued given stable core cash flows and the strategic upside of the maglev. However, the re-rating catalyst will likely require visible progress in the project timeline and inbound travel recovery.

Bull Case: Accelerated resolution of the Shizuoka section impasse, stronger-than-expected inbound demand, and early maglev monetization could drive a multiple expansion toward ~10x P/E.

Bear Case: Extended delays, cost overruns, or demand weakness in business travel could push valuation toward historical troughs (~7x P/E).

Verdict:

A high-quality infrastructure asset trading at a discount, offering long-term growth optionality for patient, risk-tolerant investors. Near-term returns may remain muted until maglev uncertainties clear, but the downside appears limited given the defensive nature of the Tokaido Shinkansen franchise.

At Wasabi Info, we publish concise equity reports and market insights through our blog—

but our core value lies in providing bespoke, on-demand research for international clients.

Whether you are a private investor or a corporation, we deliver confidential, tailored intelligence designed to support strategic decisions.

Our research services include:

• Equities: In-depth analysis of Japan-listed companies not featured in the blog

• Competitor Analysis: Detailed mapping of industry rivals and market dynamics

• Market Entry Intelligence: Insights into local barriers, regulations, and competitor positioning

• Real Estate & Assets: Localized assessments for factory, hotel, or retail expansion

• Field Intelligence: On-the-ground surveys and discreet market checks unavailable through public sources

Reports are available in English, Chinese, and Japanese.

For inquiries, please contact: admin@wasabi-info.com

© Wasabi Info | Privacy Policy

Disclaimer

This report is intended for informational purposes only and does not constitute investment advice. The analysis contains forward-looking statements and interpretations based on publicly available information as of the date of writing. Readers should conduct their own research and consult with a licensed financial advisor before making any investment decisions.

Wasabi-Info.com shall not be held liable for any loss or damage arising from the use of this report or reliance on its contents.