Konoshima Chemical Co.,Ltd. (TSE: 4026): Stock Analysis

August 12, 2025

1. Introduction

Konoshima Chemical Co., Ltd. (“Konoshima”) is a Japan-based chemical and building materials manufacturer with a history dating back to 1917. The company operates two main segments:

Building Materials — Non-combustible siding, eaves boards, and fire-resistant panels for residential and non-residential markets.

Chemicals — Primarily magnesium-based products (oxidized and hydrated magnesium for industrial and health applications) and high-performance ceramics for optical and laser applications.

Konoshima is notable for its integrated approach to material innovation, leveraging hybrid technology between its building materials and chemicals divisions. The company is actively pursuing CO₂ capture and recycling technologies, aiming for zero CO₂ emissions at its own plants by 2030.

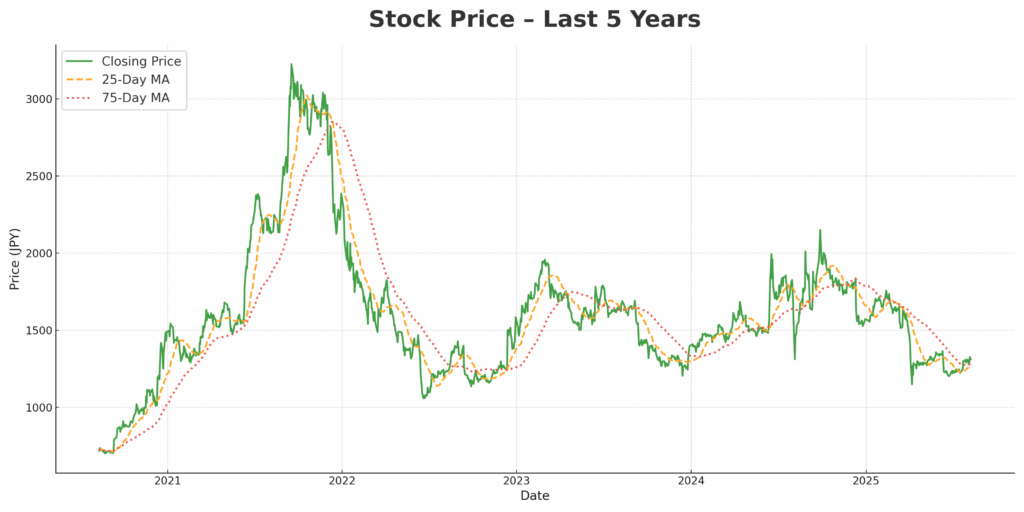

2. Stock Price Development

Over the past five years, Konoshima Chemical’s share price has experienced pronounced volatility, reflecting both company-specific developments and broader market trends.

2020–2021:

The stock began 2020 in the ¥700–¥800 range, maintaining a relatively stable trajectory amid moderate trading volumes. During late 2020 and early 2021, the share price started an upward trend, supported by steady earnings in its core refractory and industrial materials businesses, alongside optimism over infrastructure demand recovery following COVID-19 disruptions. By early 2021, the price exceeded ¥1,500.2021–2022:

Momentum accelerated through mid-2021, with the stock peaking above ¥3,000 in late 2021—marking its highest level in the past decade. This surge was driven by strong earnings growth, favorable raw material cost conditions, and heightened investor interest in industrial material suppliers amid construction sector expansion. However, by early 2022, the share price corrected sharply to the ¥1,500–¥1,800 range as profit-taking set in and global macroeconomic headwinds, including raw material price volatility, began to weigh on sentiment.2022–2023:

The stock traded in a relatively lower range of ¥1,200–¥1,700, reflecting a normalization of earnings after the post-pandemic construction rebound. While the company maintained profitability, investor enthusiasm cooled amid concerns over cost pressures and slower demand growth in certain end markets. The 75-day moving average remained below its 2021 peak levels, indicating a loss of strong upward momentum.2023–2024:

Share prices staged a partial recovery in early 2023, briefly approaching ¥1,900 on renewed optimism for industrial investment. However, this was short-lived, and by late 2023, the price trended back toward ¥1,500, as market conditions stabilized without clear catalysts for growth.2024–2025 (Year-to-Date):

In early 2024, the stock rose again to around ¥1,800–¥1,900 but encountered renewed selling pressure. The most recent months have seen a decline to the ¥1,300 range, with the 25-day moving average dipping below the 75-day moving average—a technical signal often interpreted as short-term bearish. This downtrend aligns with investor caution regarding earnings visibility and potential raw material cost increases.

Key Observations:

The stock has exhibited a cyclical pattern, with sharp rallies followed by prolonged corrections.

Price peaks coincided with periods of strong earnings reports and sector-wide optimism, while declines often followed cost concerns and macroeconomic uncertainty.

Over the long term, despite volatility, the share price remains significantly above its pre-2020 levels, indicating that market valuation has structurally re-rated the company upward compared to its historical baseline.

3. Financial and Operational Analysis (2023–2025)

3.1 Snapshot (M JPY)

| Year (FY end Apr) | Net Sales | Operating Profit | Ordinary Profit | Net Income | EPS (JPY) | DPS (JPY) |

|---|---|---|---|---|---|---|

| 2025 | 27,405 | 1,786 | 1,718 | 1,433 | 158.16 | 44.00 |

| 2024 | 25,974 | 2,117 | 2,073 | 1,620 | 179.06 | 42.00 |

| 2023 | 23,986 | 2,167 | 2,142 | 1,533 | 169.64 | 40.00 |

3.2 Key Ratios & Growth

| Year (FY end Apr) | YoY Sales Growth | Operating Margin | Ordinary Margin | Net Margin | EPS YoY | DPS YoY | Payout Ratio* |

|---|---|---|---|---|---|---|---|

| 2025 | +5.5% | 6.5% | 6.3% | 5.2% | -11.7% | +4.8% | 27.8% |

| 2024 | +8.3% | 8.2% | 8.0% | 6.2% | +5.6% | +5.0% | 23.5% |

| 2023 | — | 9.0% | 8.9% | 6.4% | — | — | 23.6% |

*Payout Ratio = DPS / EPS.

Two-year sales CAGR (2023→2025): ~6.9%.

Commentary

Top line: Sales rose for two consecutive years (+8.3% in 2024, +5.5% in 2025), reaching a record ¥27.4bn in 2025 (FY end Apr).

Margins: Profitability compressed as costs outpaced revenue growth. Operating margin declined from 9.0% → 8.2% → 6.5% (2023–2025). Ordinary and net margins followed the same trend (8.9% → 8.0% → 6.3%, 6.4% → 6.2% → 5.2%).

Earnings: Net income moved ¥1.53bn → ¥1.62bn → ¥1.43bn; EPS dipped 11.7% in 2025 after rising 5.6% in 2024—consistent with the margin squeeze despite higher sales.

Shareholder returns: DPS increased every year (¥40 → ¥42 → ¥44). The payout ratio stepped up into the high-20% range in 2025 (27.8%), reflecting a progressive dividend stance even as earnings softened.

Implication: The company is successfully growing revenue but faces margin pressure. Priorities for the near term are cost discipline, mix/pricing improvement, and capturing operating leverage so that sales growth translates more fully into profit growth, while maintaining a balanced (≈24–28%) payout policy.

4. Strategic & Technological Positioning

Dual-engine portfolio

Building Materials: focus on high-end eaves boards and siding for residential; selective push into non-residential panels. FY2025 segment sales grew +6.7% YoY while non-residential was soft on project delays.

Chemicals: Magnesium grew +5.9% YoY with overseas revenue ~56.7%; Ceramics declined −4.6% YoY on laser-related weakness and inventory disposals affecting margin.

Mid-term pillars (FY2026–FY2028):

CO₂ circular products / “Zero CO₂ at plants by 2030.” Capture plant CO₂ and embed it into products; expand practical CO₂ recycling across use-cases.

High-end ceramics for optical devices and high-power lasers (including fusion-related markets) — a structural margin lever if volumes normalize.

AI / KIP productivity program to lift throughput and offset labor constraints.

Competitive angle: A century-old materials base, hybridization between building materials × chemicals, and niche strengths in high-purity magnesium and specialized ceramics support differentiation through cycles. FY2022–FY2024 capex built capacity, particularly for magnesium and ceramics, positioning for the next upcycle.

5. Risks & Catalysts

Key risks:

Domestic housing exposure: structural headwinds from demographics; volatility in housing starts can impact building materials.

Raw materials / energy inflation and FX could pressure margins.

Ceramics demand cyclicality (laser/optical) and inventory actions can swing profitability.

Execution risk around CO₂ recycling commercialization and new product adoption timelines.

Potential catalysts:

Recovery in high-power laser/optical ceramics orders; utilization ramp on new lines.

Evidence of CO₂-fixation products gaining customer traction (pricing power / mix).

Continued overseas magnesium growth (supplements / flame-retardants).

Operating leverage from AI/KIP efficiency gains.

6. Conclusion

Where we are: After a multi-year climb in sales, FY2025 delivered margin compression (OP −15.7% YoY; ROE 11.6%) largely tied to fixed-cost pressure and ceramics headwinds. The market de-rated the shares; at ¥1,313, valuation screens undemanding (P/E ~8.3×, P/B ~0.92×, yield ~3.3%) versus the company’s own historical ranges.

Thesis: Magnesium remains resilient with international mix; Building Materials is monetizing premium SKUs; Ceramics is the swing factor. If CO₂-circular products and high-end ceramics scale as planned, ROE can re-accelerate toward the mid-teens (historical peak 15.5% in FY2023).

Investment judgment:

Rating: HOLD (value-tilted), with selective accumulation. Current price embeds conservative expectations; however, confirmation of margin recovery (ceramics demand, cost absorption) is needed before a broad Buy.

Upgrade triggers: rebound in ceramics orders, tangible adoption of CO₂-fixation products lifting mix/ASP, and sustained ROE > 13%.

Downside watch-outs: prolonged domestic non-residential softness, further ceramics destocking, or renewed cost inflation.

At Wasabi Info, we publish concise equity reports and market insights through our blog—

but our core value lies in providing bespoke, on-demand research for international clients.

Whether you are a private investor or a corporation, we deliver confidential, tailored intelligence designed to support strategic decisions.

Our research services include:

• Equities: In-depth analysis of Japan-listed companies not featured in the blog

• Competitor Analysis: Detailed mapping of industry rivals and market dynamics

• Market Entry Intelligence: Insights into local barriers, regulations, and competitor positioning

• Real Estate & Assets: Localized assessments for factory, hotel, or retail expansion

• Field Intelligence: On-the-ground surveys and discreet market checks unavailable through public sources

Reports are available in English, Chinese, and Japanese.

For inquiries, please contact: admin@wasabi-info.com

© Wasabi Info | Privacy Policy

Disclaimer

This report is intended for informational purposes only and does not constitute investment advice. The analysis contains forward-looking statements and interpretations based on publicly available information as of the date of writing. Readers should conduct their own research and consult with a licensed financial advisor before making any investment decisions.

Wasabi-Info.com shall not be held liable for any loss or damage arising from the use of this report or reliance on its contents.